Houston has a high humidity and frequent storms and floods often damage the mold of the homeowners. It is a pity to note that a number of claims about mold are turned down in insurance. The knowledge of the causes of such rejection will aid you to do the necessary actions to secure your property and increase your likelihood of being granted your claim.

The reason Mold Claims are usually denied in Houston

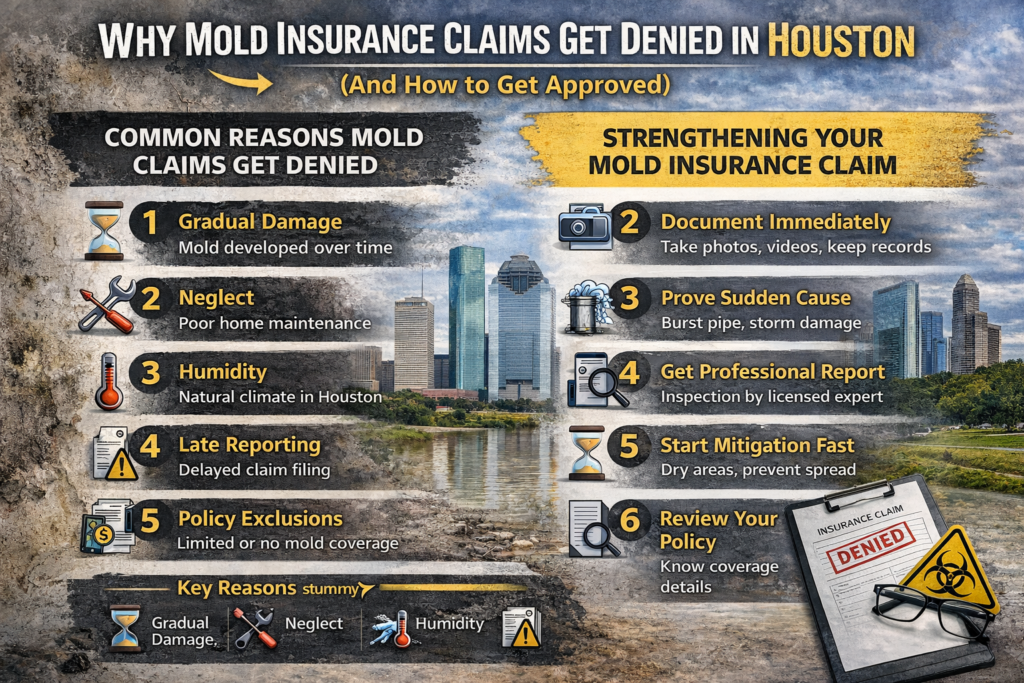

Absence of Evidence of Sudden Damage

Accidental and unexpected damage which includes the bursting of a pipe is covered by insurance policies. Mold, however, tends to grow slowly. Your claim can be rejected in case the insurer finds out that the damage was caused by time.

Poor Maintenance

One of the largest causes of claim rejection is neglect. The insurance companies can reject the claims in case they detect:

- Unrepaired leaks

- Broken rooftops not repaired.

- Poor HVAC maintenance

It is the duty of the homeowner to have the house taken care of on a regular basis.

Houston’s Natural Humidity

The climate in Houston boasts of humidity. The insurers can claim that humidity caused the mold, which was an expected environmental factor and not an accident.

Delayed Reporting

The majority of insurance policies demand urgent reports of damages by the homeowners. Late filing of a claim may result in:

- Suspicion of neglect

- Reduced compensation

- Full claim denial

Limited or Excluded reimbursement

Many policies either:

- Limit mold coverage (e.g., $5,000-$10,000), or

- Also omit the damage of mould, unless it is showcased.

Key Reasons at a Glance

| Reason for Denial | Explanation | Impact on Claim |

| Gradual Damage | Mold developed over time | High denial risk |

| Negligence | Lack of maintenance | Claim rejected |

| Humidity Conditions | Considered normal in Houston | Limited coverage |

| Late Reporting | Delay in notifying insurer | Reduced payout |

| Policy Exclusions | Mold not covered or capped | Partial/zero payout |

How to Build Your Case on Mold Insurance

Record All Things as They Happen

Take photos and videos of:

- The source of water damage

- Affected areas

- Visible mold growth

Record and keep time stamps to prove.

Prove the Cause Was Sudden

It is necessary to emphasize the fact that the mold appeared because of:

- Burst pipes

- Storm damage

- Appliance leaks

This is necessary in order to approve claims.

Receive Professional Inspecting Reports

Employ licensed mold examiners or restorers to give:

- Detailed reports

- Cause identification

- Damage assessment

Professional documentation is a plus of credibility.

Act Quickly

Begin mitigation on a timely basis:

- Remove standing water

- Use dehumidifiers

- Dry affected areas

Responsibility is demonstrated by fast action and prevents additional harm.

Check Your Insurance Policy

Know your policy information, such as:

- Coverage limits

- Exclusions

- Claim deadlines

In case of necessity, refer to a public adjuster.

Homeowner Pro Tips in Houston

- Check your house often to see whether it has any leaks.

- Keep roofing and plumbing systems.

- Dehumidify during humid seasons.

- Bathrooms and kitchens should be well ventilated.

Prevention eliminates risk of mould as well as chances of claims denial.

If you’re facing mold damage or water-related issues in Houston, Pro Texas provides expert restoration and inspection services to protect your property. Their team helps identify the source, prevent further damage, and guide you through the insurance claim process with proper documentation, ensuring a stronger and more successful claim outcome.

Conclusion

Claims on mold in Houston are usually rejected because of the slow damages, bad maintenance, or insurance restrictions. But you can really increase your chances of getting the approval by documenting evidence, acting fast, and demonstrating that you have suffered a sudden cause. The most important thing in securing your house and your money is being self-protective and knowledgeable.